Capital Markets Memorandum 002

by: Eli FieldsPublished on: 28/04/2026

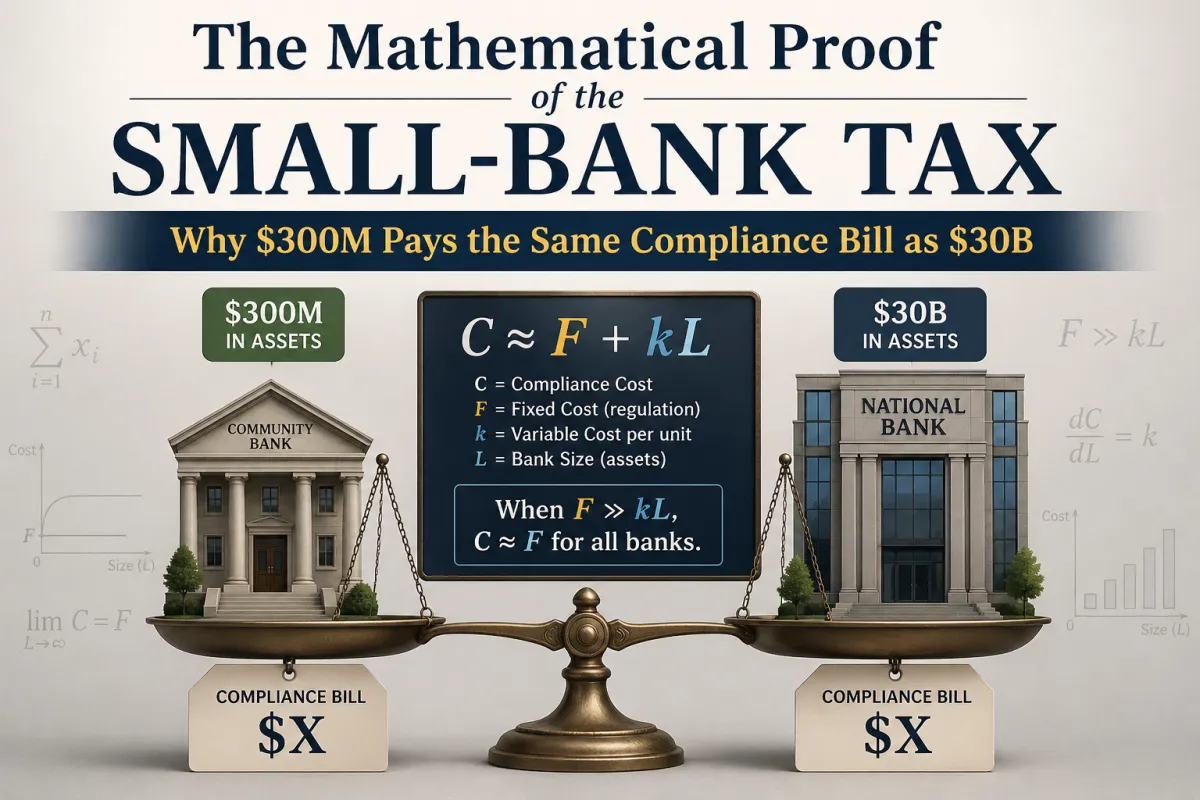

by: Eli FieldsPublished on: 28/04/2026The first analytical point is definitional: the core operating costs of a regulated depository institution do not scale linearly with asset size. They are, in the language of cost accounting, predominantly fixed

Capital Markets Memorandum